Bank Reconciliation for Sole Traders and Freelancers

Bank Reconciliation for Sole Traders and Freelancers in Australia

In Australia, where taxation policies are strict and financial records must be accurate, keeping track of all income and expenses is essential. However, many sole traders and freelancers occasionally lose receipts or forget to record small transactions. This is why bank reconciliation for sole traders and freelancers is important. It ensures that your accounting records match the actual activity shown in your bank statement.

Traditional bank reconciliation is usually performed manually. This involves comparing bank statements with accounting records or spreadsheets, which can be time-consuming and prone to human error. A 2025 survey suggested that more than 60% of small businesses spend up to two days each month performing reconciliation tasks. Fortunately, modern accounting tools and automation can simplify this process significantly.

In this guide, we will explain the basics of bank statement reconciliation, why it matters for freelancers and sole traders, the step-by-step process, and the common mistakes you should avoid.

Understanding Bank Reconciliation for Sole Traders

Bank reconciliation, also known as bank statement reconciliation, is the process of comparing your accounting records with the transactions recorded in your bank statement. If both records contain the same transactions and balances, your accounts are considered reconciled.

For freelancers and sole traders, reconciliation helps ensure that all income, expenses, and payments are recorded correctly. Many business owners rely on small business accounting software in Australia such as Xero, QuickBooks, or other accounting apps to automate reconciliation. These tools can automatically import bank transactions and match them with your financial records.

However, even with automation, it is important to understand the reconciliation process so you can identify mistakes or discrepancies early.

Why Bank Reconciliation Is Important

Performing regular bank reconciliation helps you maintain accurate financial records and avoid accounting issues. Here are some key benefits:

- It helps you confirm the exact amount of money available in your business account.

- You can identify duplicate transactions or potential bank errors.

- It helps detect suspicious or fraudulent transactions early.

- Reconciled records ensure accurate reporting for taxation and BAS lodgement.

- Tracking cleared and pending transactions reduces the risk of accidental overdrawing.

Common Errors During Bank Reconciliation

Before performing reconciliation, it is helpful to understand the most common errors that can occur. Even small mistakes can affect cash flow, financial reports, and tax compliance.

- Accepting imported bank transactions without verifying supporting invoices.

- Recording payments directly instead of allocating them to supplier bills.

- Incorrectly classifying GST-registered transactions.

- Creating duplicate supplier or customer records.

These errors can lead to incorrect BAS reporting, inaccurate expense records, and potential compliance risks.

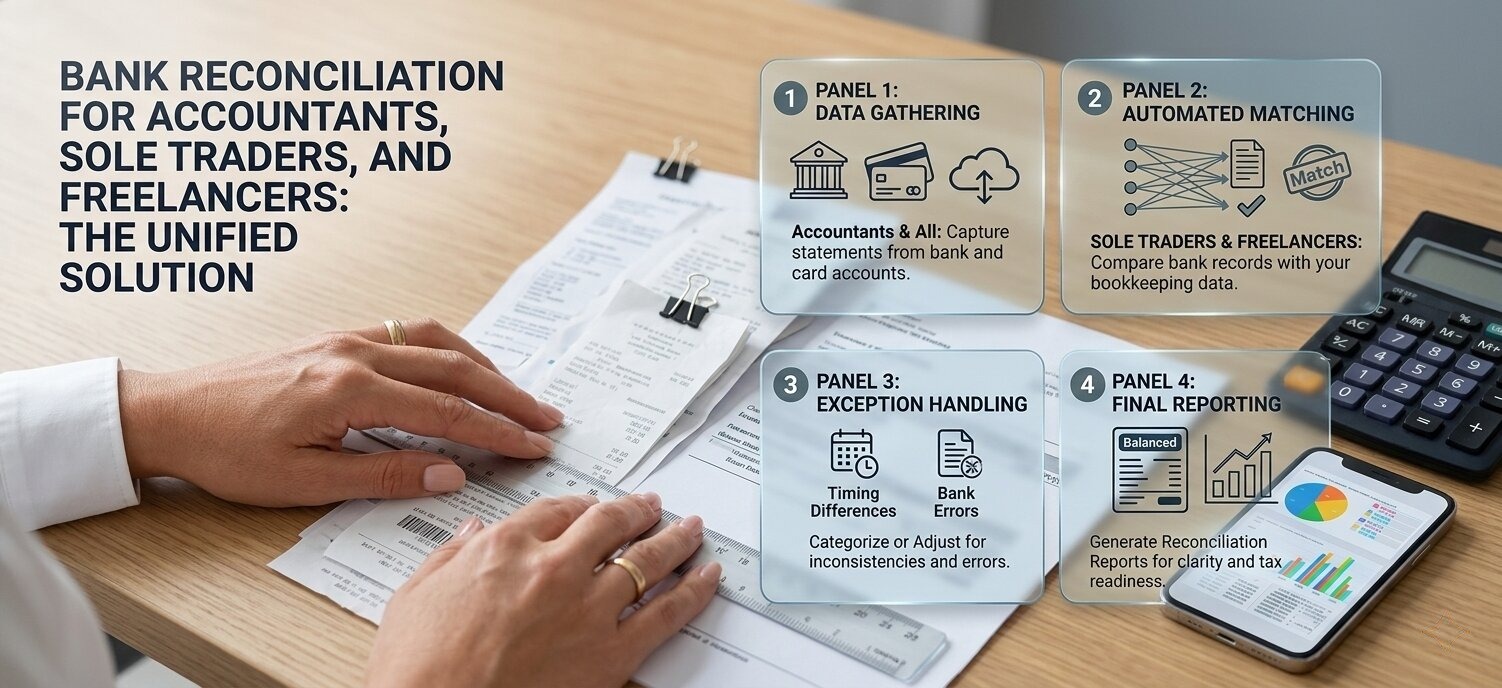

Step-by-Step Bank Reconciliation Process

Below is a simple process for performing bank reconciliation for freelancers and sole traders.

Step 1: Gather Your Financial Records

Start by collecting all relevant financial records. These may include invoices, receipts, income records, and your bank statement for the period you want to reconcile.

Step 2: Verify the Opening Balance

The opening balance in your accounting records must match the opening balance in your bank statement. If these numbers do not match, reconciliation will be difficult.

Step 3: Compare Transactions

Next, compare every transaction listed in your accounting records with your bank statement. This may include:

- Deposits

- Sales revenue

- Refunds

- Business purchases

- Payroll expenses

- Interest charges

- Bank fees

This step is crucial because it helps you identify discrepancies early.

Step 4: Make Necessary Adjustments

If you discover missing or incorrect transactions, adjustments must be made. Possible adjustments include:

- Adding deposits that have been recorded in your books but not yet processed by the bank.

- Subtracting cheques or payments that have been issued but not yet cleared.

- Correcting any errors or omissions in your accounting records.

- Investigating differences before making changes.

Step 5: Adjust Your Cash Account

You may also need to update your accounting records for bank-related items such as:

- Bank service charges or transaction fees.

- Interest earned or charged by the bank.

- Returned or NSF (Not Sufficient Funds) cheques.

- Posting errors discovered during reconciliation.

Step 6: Confirm the Closing Balance

Finally, confirm that the closing balance in your accounting records matches the closing balance in your bank statement. This balance will become the opening balance for the next reconciliation period.

Common Challenges in Bank Reconciliation

Sole traders and freelancers may face several challenges when performing reconciliation.

Unrecorded Deposits

Some deposits may still be in transit and not yet appear in your bank statement. This can temporarily create mismatched balances.

Uncleared Cheques

Cheques issued to suppliers may not be processed immediately by the bank, causing differences between records.

Unexpected Bank Charges

Unexpected bank fees such as overdraft charges, transaction costs, or service fees can affect reconciliation if not recorded promptly.

Challenges Without Automation

Manual reconciliation using spreadsheets can be slow and prone to mistakes. Many business owners now use accounting software for sole traders in Australia to automate reconciliation and reduce errors. Modern accounting apps can automatically import bank feeds and match transactions, saving time and improving accuracy.

FAQs

How often should you perform bank reconciliation?

Ideally, reconciliation should be performed weekly to keep financial records accurate. At a minimum, it should be done monthly.

What happens if reconciliation is delayed?

Delayed reconciliation can lead to forgotten transactions, late supplier payments, incorrect BAS lodgements, and missed tax deductions.

What is the formula for bank reconciliation?

Adjusted Bank Balance = Bank Statement + Deposits in Transit − Outstanding Cheques ± Bank Errors

Adjusted Cash Account = Ledger Balance − Bank Fees + Interest − NSF Cheques ± Accounting Errors

Conclusion

Bank reconciliation is essential for maintaining accurate financial records and ensuring the financial health of your business. For freelancers and sole traders in Australia, consistent reconciliation helps maintain reliable financial reports, manage cash flow effectively, and remain compliant with ATO requirements. By performing regular reconciliation and using modern accounting tools, business owners can gain better financial clarity. Learn more about bank statement scanning software that can automate this process, reduce errors, and make informed decisions for their business growth.